Legal Matters: Debt Collection, EPoA vs AHD & The Cost of Wills

In this episode of Legal Matters on 4CRB, Andrew Bell and Colin Balewski celebrate a significant personal milestone for Bell & Senior Lawyers before taking a deep dive into the practical legal world of personal debt collection, estate planning documents, and the real cost of securing your final wishes.

The episode field lives listener calls covering Enduring Powers of Attorney and Advance Health Directives under the Powers of Attorney Act 1998 (Qld) , the dangers of codicils under the Succession Act 1981 (Qld) , the mechanics of personal debt recovery through QCAT and the Queensland courts, and how to use the Personal Property Securities Register under the Personal Property Securities Act 2009 (Cth) to secure a private loan against a vehicle.

Key Topics

- Becoming a Lawyer in Queensland: Andrew explains the five step process of being admitted to the Supreme Court of Queensland, from completing a law degree through to the formal admissions ceremony.

- EPoA vs Advance Health Directive: How the two documents interact under the Powers of Attorney Act 1998 (Qld), which one overrides the other for specific medical decisions, and why both may be appropriate depending on your circumstances.

- The Problem with Codicils: Why adding supplementary pages to an existing Will under the Succession Act 1981 (Qld) is a practical and legal trap, and why a fresh Will is almost always the better approach.

- Personal Debt Collection: The evidence required to recover a personal loan in court, why verbal loans are notoriously difficult to enforce, and how text messages and bank records can constitute written evidence.

- Securing a Loan with the PPSR: How to use the Personal Property Securities Register to register a security interest against a vehicle for a personal loan, what a PPSR search reveals to a buyer, and why it costs only a few dollars to protect thousands.

- Closing an SMSF: When closing a self managed superannuation fund is purely an accounting matter and when a solicitor’s involvement is actually required.

Listener FAQ Highlighted in This Episode

- Enduring Power of Attorney vs Advance Health Directive in Queensland

- Should I use a codicil to update my Will in Queensland?

- How much does a Will cost in Queensland?

- How do I collect a personal debt in QCAT?

- What is the Personal Property Securities Register?

Listen to the full discussion above.

Verbal Loans Are Almost Impossible to Enforce

If you loan money to a friend or family member without a written agreement, recovering it in court becomes a case of your word against theirs. The civil standard of proof requires you to demonstrate it is more likely than not that money changed hands and was intended to be repaid, not given as a gift. Always put loan agreements in writing, clearly define the repayment schedule, and keep a record of the bank transfer. Even a confirming text message creates a contemporaneous written record that a court can rely upon.

Contact our commercial litigation team today to draft a binding loan agreement or to pursue recovery of an outstanding debt. Call (07) 5532 8777.

Key Takeaways

- Advance Health Directives override an EPoA for specific medical decisions. Under the Powers of Attorney Act 1998 (Qld) , if your Advance Health Directive and your Enduring Power of Attorney give conflicting instructions about a specific medical treatment, the medical team must follow the Advance Health Directive. Your documented medical wishes take legal precedence over your attorney’s discretion for those covered decisions.

- Avoid codicils: draft a fresh Will instead. Codicils under the Succession Act 1981 (Qld) are easily lost, separated from the original Will, or the subject of disputes about execution formalities. A new Will that expressly revokes all previous Wills and codicils eliminates ambiguity and keeps the testamentary record clean.

- Get loans in writing, even informally. The civil standard of proof requires you to demonstrate it is more probable than not that money was a loan rather than a gift. Text messages, emails, and bank transfer descriptions all constitute contemporaneous written evidence a court can rely on.

- Use the PPSR to secure a vehicle loan. Under the Personal Property Securities Act 2009 (Cth) , a PPSR registration against a vehicle’s VIN costs around $7.40 for a seven year registration and protects your interest if the borrower becomes insolvent or attempts to sell the vehicle. Anyone conducting a PPSR search before purchase will see your registered interest.

- Know your court: QCAT for debts up to $25,000. Debts up to $25,000 can be pursued through QCAT without a lawyer, under the Queensland Civil and Administrative Tribunal Act 2009 (Qld) . Between $25,000 and $150,000, file in the Magistrates Court under the Magistrates Courts Act 1921 (Qld) . Between $150,000 and $750,000, file in the District Court. Above $750,000, file in the Supreme Court of Queensland.

- A court order is not automatic payment. Winning a judgement in any Queensland court or QCAT does not mean the money arrives immediately. You must then enforce the judgement, which may involve default interest, a bailiff, forced sale of assets, or bankruptcy proceedings. Queensland judgement debts carry a six year limitation period for enforcement.

Annotated Transcript

Topic: Admission to the Legal Profession in Queensland

The requirements for admission as a legal practitioner under the Legal Profession Act 2007 (Qld) and the Supreme Court (Admission) Rules 2004 (Qld).

Announcer: 4CRB now presents Legal Matters, proudly brought to you by Bell & Senior Lawyers. Call them today for all your legal needs on 07 5532 8777. This program provides general legal information only. It is not personal legal advice. Everyone’s situation is different, so please seek independent advice for your own circumstances.

Colin: And it is a very good morning to Andrew Bell from Bell & Senior Lawyers. Good morning to you, Andrew.

Andrew: Good morning, Colin. Thanks for having me back. I would like to welcome everyone to Legal Matters and acknowledge our wonderful new sponsor, Bell & Senior Lawyers.

Colin: I believe you have a good news story to share this morning. Your lovely wife has just been admitted to the bar.

Andrew: Absolutely. Yesterday I had the genuine pleasure of moving my wife Rebecca to be admitted to the legal profession in a ceremony in the Supreme Court of Queensland. She has been working on that for a long time. She has been studying law while raising five girls. She started this process before our youngest was even crawling, and that girl is just about to turn five years old. That is a level of dedication that most people cannot imagine, and I am very proud of her.

Colin: That is absolutely fantastic, especially raising a family at the same time. What does it actually take to become a lawyer in Queensland?

Andrew: It is a more involved process than people realise. There are essentially five stages. The first is completing a recognised law degree at an accredited Australian university, which takes three to five years of full time study. Once you have that degree, you complete a period of practical legal training, where you work in a law firm and are assessed on the practical application of the law, not just the academic theory. After that, you go through the admissions process with the Legal Practitioners Admissions Board, which involves submitting detailed paperwork, affidavits about your character and background, and satisfying both the technical and the moral requirements for admission. If the Board is satisfied, you then make an application to the Supreme Court of Queensland, who make the ultimate decision on admission. Finally, at the admission ceremony itself, a practising barrister or solicitor formally moves that you are a fit and proper person to be admitted.

Colin: A fit and proper person. I assume that means both academic and moral requirements?

Andrew: Yes. You have to make full disclosure of anything relevant to your character, whether it relates to tax obligations, any fines you have received, or any prior disciplinary proceedings. The Board assesses all of that to determine whether you meet the standard. Lawyers are in a position of enormous trust. Clients tell us their deepest secrets, and we carry strict obligations of confidentiality. We also hold an obligation to the court itself not to mislead it in any proceedings. The character requirements exist to protect the public and to maintain the integrity of the profession.

Topic: Advance Health Directives vs Enduring Powers of Attorney

Applying the Powers of Attorney Act 1998 (Qld) , ss 32, 35, and 36.

📎 See also: Enduring Power of Attorney vs Advance Health Directive in Queensland

Colin: We have our first caller this morning. Good morning to Jeffrey. Ask your question of Andrew.

Jeffrey: Good morning, Andrew. Thank you for taking the time. I am preparing an Enduring Power of Attorney and I would like your opinion on whether there is any benefit to also having an Advance Health Directive, given that my Enduring Power of Attorney will include both health and financial matters.

Andrew: That is an excellent question, Jeffrey. Let me explain how the two documents work together under Queensland law. An Enduring Power of Attorney, under the Powers of Attorney Act 1998 (Qld) , appoints someone you trust as your attorney to make decisions on your behalf when you no longer have capacity. That appointment can cover financial matters, personal matters, and health matters, and it endures even after you lose capacity, which is what makes it an enduring power rather than a general power.

An Advance Health Directive is a different document under the same Act. You sign it with your doctor present, and it records your specific directions about particular medical treatments: what you do want, what you do not want, and under what circumstances. It is more than an appointment of an attorney. It is a direct expression of your own instructions about your medical care.

Jeffrey: I suppose I was thinking about what happens if I have an accident that could happen at any age. If my Enduring Power of Attorney sets out my wishes for medical matters, would the people treating me actually know about it and contact my attorney?

Andrew: That is the practical consideration. It depends entirely on whether the treating medical staff know how to contact your attorney. Carrying something in your wallet, your phone, or your medical records that identifies who your attorney is and how to reach them is an important practical step. In an emergency, if Queensland Health cannot quickly locate or contact your attorney, they may be required to make treatment decisions without that input.

An Advance Health Directive, once made, is kept on file with Queensland Health. If you are admitted to hospital in an emergency and staff run your records, your directive will be accessible to them directly. That is a significant practical advantage over an Enduring Power of Attorney alone, particularly for urgent medical decisions.

The important legal point to be aware of is this: if you have both documents, you must ensure the directions you give in your Advance Health Directive are consistent with the authority and instructions you have given your attorney in the Enduring Power of Attorney. If there is a conflict between them, the law is clear.

Jeffrey: That is exactly what I was confused about. If both exist and they conflict, which one wins?

Andrew: The Advance Health Directive wins, for the specific medical decisions it covers. Under the Powers of Attorney Act 1998 (Qld) , an Advance Health Directive legally overrides an Enduring Power of Attorney for those specific medical decisions recorded in the directive. Your documented medical instructions take precedence over your attorney’s discretion. The medical team is required to follow the Directive. For any health decisions not covered by the Directive, your attorney under the Enduring Power of Attorney resumes their authority.

An Advance Health Directive under the Powers of Attorney Act 1998 (Qld) must be signed by the adult principal, a doctor who has explained the document and the principal’s medical circumstances, and an eligible witness such as a justice of the peace, commissioner for declarations, notary public, or lawyer (s 44). It can only be revoked while the principal has legal capacity (s 42). Attempting to rely on a directive that conflicts with your Enduring Power of Attorney, without resolving that conflict in advance, creates precisely the legal uncertainty this episode discusses.

Visit our Wills & Estates practice page for further information about Powers of Attorney and Advance Health Directives in Queensland.

Topic: Codicils vs New Wills

Applying the Succession Act 1981 (Qld) regarding testamentary amendments and revocation.

📎 See also: Should I use a codicil to update my Will in Queensland?

Colin: All right, moving on to John. Ask your question of Andrew.

John: Good morning. My question is: is it a good idea to add a codicil to an existing Will, or should I get a new Will prepared?

Andrew: A codicil, for those listening who may not be familiar, is a separate legal document that amends or supplements an existing Will without replacing it entirely. They were much more common in earlier generations when preparing a Will was a laborious process. The codicil had to be executed with the same formalities as the Will itself, including two witnesses, but it allowed small changes to be made without redrafting the entire document.

Our strong recommendation to clients today is not to use them, and to draft a fresh Will instead. The practical reason is exactly what John has touched on: codicils are easily separated from the original Will document, easily misplaced, and when they are found separately from the Will they raise immediate questions about whether they were validly executed, whether they were revoked, and whether they accurately reflect the testator’s final intentions. A codicil that cannot be located with the original Will may be presumed by a court to have been intentionally destroyed and revoked. That uncertainty is expensive and distressing for the estate to resolve.

A new Will that expressly revokes all prior Wills and codicils eliminates every one of those problems. It is a single, clean document that represents the testator’s current intentions without ambiguity. For the modest additional cost of having the document drafted fresh, it removes any room for dispute.

John: There were only two small things I wanted to change, but I can see your point entirely. I will go ahead with a new Will. Is the correct pronunciation codicil, not cordicil?

Andrew: It is codicil, with a soft c. An easy one to mispronounce. Thank you, John.

Under the Succession Act 1981 (Qld) , a Will is only revoked by marriage, divorce, or the execution of a new Will that expressly revokes the prior Will. A codicil that conflicts with a prior Will operates as a partial amendment only for the matters it specifically addresses. If you have an existing Will with a codicil attached, your solicitor should review both documents together to confirm the combined testamentary intention is clear and internally consistent.

Visit our Wills & Estates practice page for information about Will preparation, codicils, and estate planning in Queensland.

Topic: Personal Debt Collection and the PPSR

Procedures for recovering personal loans and registering security interests under the Personal Property Securities Act 2009 (Cth) .

📎 See also: What is the Personal Property Securities Register?

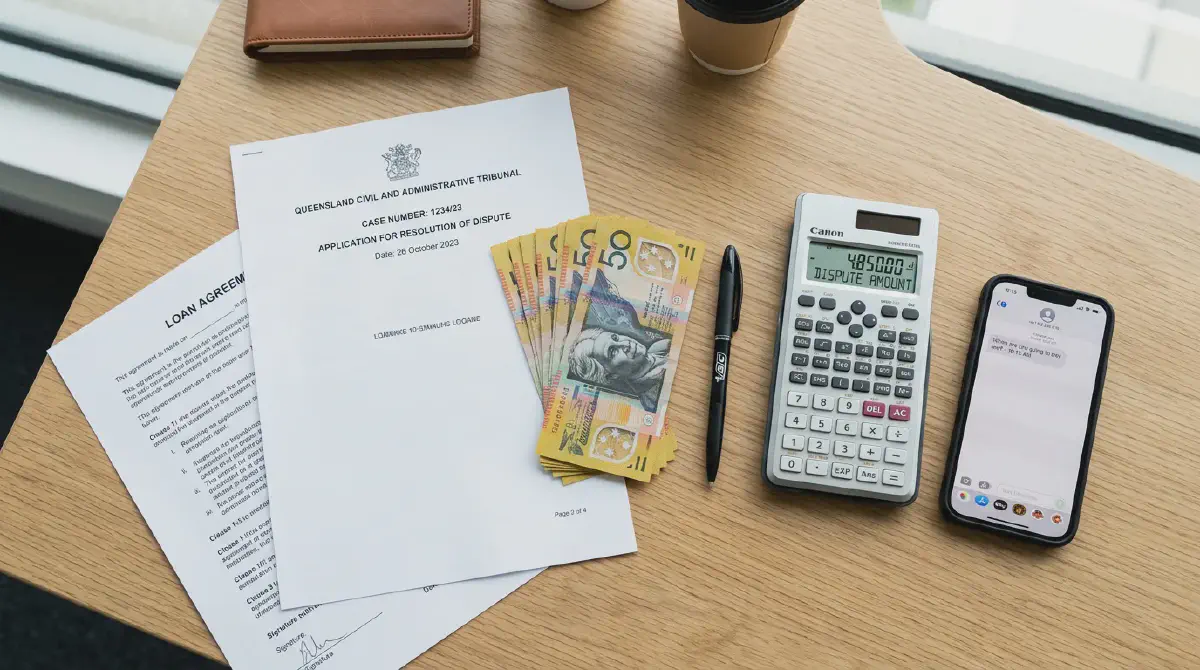

Colin: Our main topic today is debt collection. Let us start simply. Someone owes me money. What do I do?

Andrew: This comes up very frequently. At the community legal centre it is one of the most common questions I am asked, usually framed as: I loaned money to someone and they are not paying it back.

My first question is always about the circumstances of the loan. To enforce a debt in court, the arrangement needs to be sufficiently certain: you need to be able to prove that money changed hands and that there was a genuine intention on both sides that it would be repaid. Was there a written agreement? Is there any written evidence before or after the transfer that records what was agreed? Even a text message exchange confirming the amount, the purpose, and the expectation of repayment is evidence.

Without that evidence, debt recovery can be very difficult. Businesses lending money always document their terms precisely. For personal loans, I strongly recommend that anyone lending money to a friend or family member asks them to confirm the arrangement in writing, even informally. A simple text message saying please confirm you want $1,000 lent to you and that you will repay it within six weeks is a contemporaneous record that a court can rely on.

Colin: It is uncomfortable asking family and friends for written agreements. But people’s circumstances change in ways nobody predicts.

Andrew: Absolutely. And without written evidence, if you want to go to QCAT or the Magistrates Court to recover the money, it becomes extraordinarily difficult. If you say I lent you $5,000 and they say that was a gift, how do you disprove that? You need to satisfy the civil standard of proof, which requires demonstrating it is more probable than not, that is, 51% likely or greater, that the money was a loan and not a gift. Text messages, bank transfer records showing the transaction, and any messages discussing repayment all help establish that probability.

Colin: What if the loan was secured against a physical asset like a car or other property?

Andrew: This is done routinely in business lending but is rarely done in personal lending, and that is a missed opportunity. What security means in a legal sense is that a physical asset owned by the borrower can be sold or transferred to satisfy the debt if they do not repay.

Most people have not heard of the PPSR, the Personal Property Securities Register, established under the Personal Property Securities Act 2009 (Cth) . It is a national online register where you can register a security interest against a specific asset, most commonly a motor vehicle identified by its VIN number. If anyone is buying a used car, I strongly recommend conducting a PPSR search first. It currently costs around $2 to $3 for a search. The search will tell you whether any finance company, lender, or private individual has a registered security interest against that vehicle.

The critical legal effect of a PPSR registration is this: if the borrower sells the car without your consent or enters bankruptcy, your registered security interest travels with the asset and takes priority. The person who bought the car from the borrower does not get a clean title if there is a registered security interest they could have discovered by searching. Your interest in the debt is legally protected.

Topic: The Cost of Drafting a Will in Queensland

Comparing DIY Will kits, the Public Trustee of Queensland, and private solicitor fees.

📎 See also: How much does a Will cost in Queensland?

Colin: We have another caller this morning. Good morning to Robert. Ask your question of Andrew.

Robert: I just have a simple question about a basic Will. What sort of price would it cost in Queensland?

Andrew: It really depends where you go to have it prepared, Robert, and each option carries a different risk and cost profile.

The least expensive option is a do it yourself Will kit from Australia Post, which costs around $32. The risk with those is that the formal execution requirements under the Succession Act 1981 (Qld) are easy to get wrong if you are not familiar with them. A Will that has not been properly signed and witnessed in the correct order, or that has alterations made after execution without being re executed, can be declared invalid. An invalid Will means your estate passes under the Queensland intestacy rules regardless of what you wrote, which is almost certainly not what you intended.

The Public Trustee of Queensland will prepare a Will for you at no charge for the drafting itself. The trade off is that the Public Trustee charges estate administration fees when they administer the estate after death. Those fees are calculated as a percentage of the estate value and can be considerable for larger estates. I would encourage anyone considering the Public Trustee option to ask for a written schedule of their administration fees before making a decision.

A private solicitor will typically charge between $400 and $600 for a well prepared, straightforward single Will. That fee covers drafting, guidance on execution formalities, and in many cases secure storage of the original document. Given that a Will governs the distribution of everything you have spent your lifetime building, paying $400 to $600 for a document you know will be valid and effective is very modest.

Robert: That is very helpful, thank you.

A Will that is not executed in strict compliance with the Succession Act 1981 (Qld) may be declared invalid by the Supreme Court of Queensland, and your estate will then be distributed under Queensland’s intestacy rules rather than your recorded wishes. While the court has a limited discretion under s 18 of the Act to admit an informal Will to probate, this is not guaranteed and requires expensive Supreme Court proceedings at the cost of your estate.

Contact our Wills & Estates team today to prepare a valid, clearly drafted Will that reflects your intentions. Call (07) 5532 8777.

Topic: Debt Recovery Through the Queensland Court System

Jurisdictional limits and enforcement procedures under the Queensland Civil and Administrative Tribunal Act 2009 (Qld) , the Magistrates Courts Act 1921 (Qld) , and the District Court of Queensland Act 1967 (Qld) .

📎 See also: How do I collect a personal debt in QCAT?

Colin: What happens if there is no security and you still need to force repayment? How do you get a court order?

Andrew: If informal approaches, demand letters, and negotiation have all failed, your only option is to commence proceedings in the appropriate court or tribunal and obtain a judgement that can then be enforced.

The first step is gathering your evidence: everything showing that money changed hands, the circumstances of the agreement, any written acknowledgments of the debt, and the history of any partial repayments. Once you have that evidence, you need to identify the right forum based on the amount owed.

For debts up to $25,000, you can file in QCAT, the Queensland Civil and Administrative Tribunal, under the Queensland Civil and Administrative Tribunal Act 2009 (Qld) . QCAT is designed to be accessible without legal representation and legal cost recovery is generally not available, so it is most suitable for straightforward smaller debts.

For amounts between $25,000 and $150,000, you file in the Magistrates Court of Queensland under the Magistrates Courts Act 1921 (Qld) . For amounts between $150,000 and $750,000, you file in the District Court. For amounts above $750,000, you go to the Supreme Court of Queensland. Once you are in the Magistrates Court or above, legal representation is strongly advisable, both because the procedural rules are complex and because the successful party can generally recover their legal costs from the losing party by court order.

Colin: Once QCAT or a court makes an order in my favour, does the money arrive straight away?

Andrew: Unfortunately it does not, and this is the part that frustrates most people the most. Obtaining a judgement or a QCAT order means you now have a legal entitlement to be paid. But the judgement does not pay you: it just gives you the legal right to pursue the debtor through enforcement mechanisms.

If the debtor does not pay voluntarily after receiving the judgement, you then need to enforce it. The options include: garnishee orders directed to the debtor’s employer to deduct payments from their wages; a warrant for a bailiff to seize and sell the debtor’s personal property; bankruptcy proceedings for individuals, or statutory demands and winding up proceedings for companies. Default interest accrues on unpaid judgements under the relevant court rules. Enforcement costs are generally recoverable from the debtor as well, which means the total amount you can recover grows the longer they resist paying. Queensland judgement debts can be enforced for six years from the date of judgement.

Topic: Closing a Self Managed Superannuation Fund

Legal and accounting requirements for winding up a self managed superannuation fund under the Superannuation Industry (Supervision) Act 1993 (Cth) and the ATO’s SMSF wind up requirements.

Colin: We are in the final moments of the programme. Last chance. John, ask your question of Andrew.

John: I am in the process of closing my superannuation fund. Where does a solicitor come into this or what part are they involved in?

Andrew: When you say you are closing the fund, is this a self managed superannuation fund that you no longer want to administer yourself?

John: Yes, a self managed super fund.

Andrew: In most cases, closing a self managed superannuation fund is primarily an accounting and compliance exercise rather than a legal one. The trustee of the fund needs to arrange a final independent audit, lodge the final tax return with the ATO, roll the remaining balance over to a complying superannuation fund or take any benefits you are entitled to receive, and then notify the ATO that the fund is being wound up and lodge the necessary ASIC forms if the fund is structured through a corporate trustee that also needs to be wound up or deregistered.

That process is generally handled by the fund’s accountant and auditor. A solicitor does not typically need to be involved unless the fund’s trust deed contains specific legal requirements for winding up that go beyond standard ATO procedures, or unless there is a dispute between trustees about how the fund’s assets should be distributed, or unless the distribution of fund assets raises a question about the legal interpretation of the deed’s terms.

John: So the solicitor does not really come into it for a standard closure?

Andrew: Not typically. Your first call should be to your accountant. If they identify a legal question that needs a solicitor’s input, they will tell you. But for a straightforward wind up with no disputes and a clear deed, the accountant and auditor will be able to take you through the entire process.

Colin: Thank you very much for your time this morning, Andrew. I look forward to next week.

Andrew: Thank you, Colin. See you next week.

Disclaimer: This transcription provides general legal information only. It is not personal legal advice. Everyone’s situation is different, so please seek independent legal advice for your own circumstances.