Legal Matters: Loan Agreements, Debt Forgiveness & Your Rights Against Debt Collectors

In this episode of Legal Matters on 4CRB, Andrew Bell and Colin Balewski pick up where last week left off, completing their deep dive into personal debt collection and loan agreements. Andrew explains precisely what a private loan agreement must contain to be enforceable, how to retrospectively document a loan that was never put in writing, and the often-overlooked tax and Centrelink consequences of forgiving a debt. The second half of the episode covers the significant recent strengthening of legal protections against abusive debt collector conduct under the Australian Consumer Law.

Live callers ask about whether an estate held in individual name must go through probate even if it will pass to a trust, the process of dealing with a deceased mother’s mobile home where there is no Will, and what evidence can substitute for a written loan agreement in court.

Key Topics

- What a Loan Agreement Must Contain: The minimum information required to transform an informal family loan into an enforceable legal document.

- Documenting Loans Retrospectively: How a deed can legitimise a historical loan, and why a borrower’s refusal to sign retrospectively is a serious red flag.

- Family Loans and Gifts: Why the “gift” defence is more commonly raised in family loan disputes, and how a written agreement defeats it.

- Forgiving a Debt: The tax and Centrelink consequences of writing off a personal or commercial loan, and why a deed of forgiveness matters.

- Who Made the Loan Matters: How the tax treatment of forgiven debts differs depending on whether the lender is an individual, a company, or a trust.

- Debt Collector Conduct: The specific prohibitions under the Australian Consumer Law, and how to escalate a harassment complaint through the ACCC, ASIC, and AFCA.

- Probate and Individual Property: Why property held in an individual name always requires probate, regardless of how the estate is structured.

- Intestacy and Letters of Administration: What happens when there is no Will, and why applying to the Supreme Court for Letters of Administration is the only legally protected path to distributing an estate.

- Testamentary Trusts vs Lifetime Trusts: Why the type of trust changes everything about CGT and probate.

Listener FAQ Highlighted In This Episode

- What must a personal loan agreement include?

- Can I document a loan after the money has been handed over?

- Are family loan agreements legally binding in Queensland?

- What are the tax consequences of forgiving a debt?

- What is a deed of forgiveness?

- What are the rules on debt collector contact and harassment?

- When is probate required in Queensland?

- What are Letters of Administration and when do I need them?

- What evidence proves a personal loan in court?

- Can I avoid probate by putting my property in a trust?

- Can a food business operate without customer toilets in Queensland?

Listen to the full discussion above.

Verbal Loans Are Difficult to Enforce — And Forgiven Debts Can Trigger Tax

If you loan money without a written agreement, recovering it depends on assembling text messages, bank records, and other circumstantial evidence. If you later decide to forgive that debt, you may inadvertently create a Centrelink gift or a taxable event. Both scenarios are avoidable with a single page of documentation.

Contact our commercial litigation team today to prepare a binding loan agreement, a deed of acknowledgment, or a deed of forgiveness. Call (07) 5532 8777.

Key Takeaways

- Get it in writing before the money moves. A one-page loan agreement covering names, amount, date, repayment terms, and both signatures is all you need to protect a personal loan from the “gift” defence.

- It is not too late if the borrower will co-operate. A deed of acknowledgment can retrospectively formalise a historical loan and is fully admissible in court or QCAT.

- A refusal to sign retrospectively is a warning. If a borrower refuses to sign any acknowledgment of an existing loan, begin gathering every piece of evidence — bank transfers, texts, emails, witnesses — immediately.

- Partial payments are powerful evidence. Any payment that cannot be explained other than as a loan repayment strongly supports the civil standard of proof required in QCAT or the Magistrates Court.

- Who forgives the debt matters as much as the forgiveness itself. Private non-commercial debts between individuals are generally outside the CGT and commercial debt forgiveness provisions. But if a private company forgives a debt owed by a shareholder or associate, Division 7A may deem the forgiveness a taxable dividend. Get accounting advice before forgiving any debt involving a company or trust.

- Debt collectors operate under strict legal limits. They cannot contact your employer, family, or neighbours about your debts, and cannot make threats or misrepresent amounts owed. Breaching these provisions exposes the collector to civil penalties under the Australian Consumer Law, and the most serious conduct (such as threats or coercion) can also amount to criminal liability.

- Property in a sole name always requires probate. Even if all beneficiaries agree, a solicitor cannot transfer title to Queensland real estate without a Grant of Probate from the Supreme Court.

- No Will means Letters of Administration, not a shortcut. Without a Will, distributing an estate through informal agreement among family exposes everyone to potential claims of theft or improper transfer. Apply to the Supreme Court first.

Annotated Transcript

Recap of Episode 11 & Getting It in Writing

Continuing the discussion of personal debt recovery from the previous episode .

📎 See also: What Evidence Proves a Personal Loan in Court?

Colin Balewski: Good morning Andrew Bell from Bell and Senior Lawyers. We’ve been talking debt collection and loans. We got great feedback from the program last week. We didn’t quite finish the discussion, so we’re going to finish that today. Before we get into today’s topic, can you give the listeners who missed last week a quick summary?

Andrew Bell: No worries, Colin. Last week we celebrated my wife being admitted as a solicitor in the Supreme Court. We went through the difference between powers of attorney and advance health directives — the key point being that the advance health directive overrides the enduring power of attorney for the specific medical decisions it covers. We discussed codicils and wills, and why it is preferable to draft a fresh will rather than add a codicil. We looked at the cost of wills. And in terms of our main topic of debt collection, we went through what evidence you need to prove that something was a loan and not a gift, the PPSR — the Personal Property Securities Register — and the limits of where you can sue. For example, up to $25,000 in QCAT, through to the Supreme Court for amounts above $750,000.

What a Loan Agreement Must Contain

📎 See also: Personal Loan Agreement Requirements | EPoA vs Advance Health Directive (Ep 11)

Colin: Last week you said “always get it in writing.” What does that actually mean in practice?

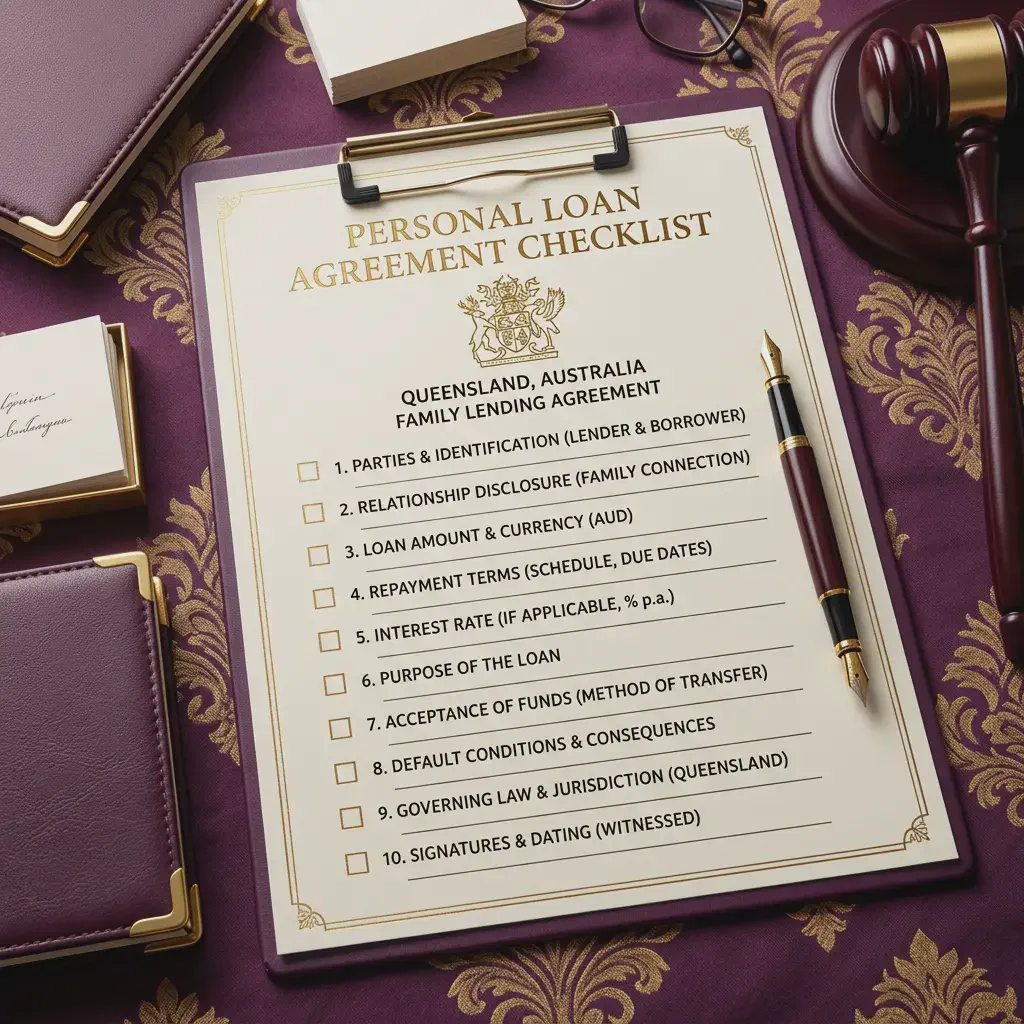

Andrew: If you are going to a bank, they will give you many pages covering all eventualities. A loan agreement between friends and family does not need to be a lengthy legal document, but if you are loaning money that you may want back, we strongly recommend putting something in writing before the money moves. At minimum, include the full names of the lender and the borrower, the principal amount being lent, the date the money was advanced, and any repayment terms — whether it is on demand, or by a specific date, whether interest applies, and what happens if the borrower misses a payment. Both parties should sign it and keep a copy. Even a one-page document covering these points transforms an informal agreement into something that is much easier to enforce if you want that money back.

Colin: Between family members, is that legally binding?

Andrew: Absolutely. Provided both parties are adults, a contract is a contract regardless of the relationship, even between husband and wife. A signed loan document between family members may actually do more good than one between strangers, because with family the defence often gets raised that the money was a gift or was never expected to come back. If you have gone to the stage of formalising it, that refutes the gift argument directly. If you are loaning large amounts or the loan is secured against a property, you may want a solicitor to prepare a full deed or loan agreement rather than a simple document, which gives you stronger evidentiary weight and more rights if you need to enforce it.

Documenting a Loan Retrospectively

📎 See also: Retrospective Loan Documentation

Colin: What if you have already handed over the money and nothing is in writing — is it too late?

Andrew: It is not too late if both parties are prepared to acknowledge the loan. You can execute a deed that acknowledges the historical amount loaned and the agreed terms. It is slightly different from a contract, but you record the original amount, the date it was lent, the repayment terms, and both parties sign it. That document is admissible as evidence in court or QCAT if the agreement is later denied.

Colin: What if the borrower refuses to sign anything retrospectively?

Andrew: Then you are starting to have a real problem. That refusal is a significant signal — it suggests the borrower knows it was a loan and is positioning themselves to deny it. My alert senses would be firing at that point. I would immediately go through every piece of evidence available: bank transfer records, text messages, emails, anyone who witnessed the advance. I would also write to the borrower formally acknowledging the loan in writing, so their response (or non-response) itself becomes part of the evidence record.

Caller 1 — Bob | Probate, Trusts & Property

📎 See also: When Is Probate Required in Queensland? | Off-the-Plan Property, Probate & Executor Powers (Ep 10)

Bob (Caller): I have a reasonable property estate. I am in my 80s and thinking seriously about my will, in which I have left the entire estate to my two children in equal shares. All my property is in my individual name. My wife and I have separated and done a BFA. Will my estate have to go through probate, and is there a smarter way to pass my property to my two children, through a trust perhaps?

Andrew: Because you own property that will transfer on your death to another party, it will have to go through probate. Whether that other party is a trust or the children personally, probate is still required to transfer Queensland real estate. Because you have executed a binding financial agreement, your former partner is very unlikely to have any rights to challenge the estate. If your children are the executors, probate is essentially unavoidable but should be straightforward.

Bob: What about transferring the properties into a trust before my death to simplify things?

Andrew: Roughly the same amount of work is going to occur either way. Importantly, there may be capital gains tax implications depending on how the properties are transferred, so I would strongly recommend speaking to an accountant before making any transfers during your lifetime. That transfer may or may not be the most tax-effective approach, and you cannot undo it once done.

Testamentary Trusts vs Lifetime Trusts: Key Differences for Estate Planning

Bob’s question touches on an important distinction that is worth understanding:

-

A testamentary trust is a trust created inside your Will that only activates upon your death. Assets still pass through probate once, but the transfer into the trust on death is exempt from CGT and stamp duty in Queensland. Beneficiaries then receive distributions from the trust with significant tax flexibility — including the ability to income-split with minor children at adult tax rates under section 102AG of the Income Tax Assessment Act 1936 (Cth).

-

A discretionary (inter vivos) trust set up during your lifetime can hold assets that bypass probate entirely, since the trust owns the assets, not you personally. However, transferring existing investment properties into a living trust triggers CGT at market value on the full capital gain to date, plus Queensland stamp duty on the transfer — potentially a very large immediate tax bill for someone who has owned property for decades.

For most Queensland residents with investment property, a testamentary trust inside a well-drafted Will delivers the asset protection and tax flexibility benefits without the upfront CGT and stamp duty cost. Speak to both a solicitor and an accountant before deciding which structure suits your circumstances.

📎 See also: When Is Probate Required in Queensland?

Caller 2 — Amber | No Will, Mobile Home & Letters of Administration

Applying the Succession Act 1981 (Qld) intestacy provisions.

📎 See also: Letters of Administration in Queensland

Amber (Caller): My mum passed away about three years ago, very quickly. She has a mobile home that my sister is currently living in. There was no will because she died within 11 days of going into hospital. It is just myself and my sister — would it be 50/50? What is the process for us to sell it?

Andrew: Without a will, this is where you encounter the problem of who has legal standing over the assets. Typically, you would need to apply to the Supreme Court for letters of administration, which appoints someone as the administrator of the estate. Without a will, the default provisions of the Succession Act apply — if there was no partner at the time of death and children survive her, the estate passes to the children in equal shares. With just two children, yes — 50/50.

Amber: Could we simply agree between us and sell it without going to court?

Andrew: That is not the process I can recommend. Without being formally appointed as administrator, you do not have legal standing to enter into transfer documents or deal with registration. The official process is to apply for letters of administration, and once appointed you can sell the asset as if it were your own and distribute the proceeds according to the rules of intestacy — equally between the two of you.

Colin: If you go through the Supreme Court and get the grant, does that fully protect you if anyone questions the distribution later?

Andrew: Completely. No one who might otherwise have inherited, and no purchaser who claims proper title was not transferred, can raise any allegation. You are fully protected. The moment there are valuable assets in an estate — and real property or a registered vehicle qualifies — doing it properly is strongly recommended.

Evidence When There Is No Written Agreement

📎 See also: What Evidence Proves a Personal Loan in Court? | Debt Collection, EPoA & Wills (Ep 11)

Colin: Can a bank statement showing money moving from your account to theirs be enough evidence?

Andrew: These matters are decided on the civil standard in court — not beyond reasonable doubt, but more likely than not. A bank transfer alone shows money moved. What helps prove it was a loan and not a gift is surrounding context: a text message saying “Yes, I will pay you back tomorrow,” a bank transfer description referencing the debt, a partial repayment. Any partial payment that cannot be explained as anything other than a loan repayment is very strong evidence. It is an implicit acknowledgment of the debt, and it significantly strengthens your case.

Forgiving a Debt: Tax & Centrelink Consequences

Applying Division 7A of the Income Tax Assessment Act 1936 (Cth) for company loans, and the Income Tax Assessment Act 1997 (Cth) CGT provisions for private debts.

📎 See also: Tax Consequences of Forgiving a Debt | What is a Deed of Forgiveness?

Colin: What if someone simply decides not to pursue a debt — are there tax consequences?

Andrew: Yes, and this catches people off guard. You are absolutely entitled to choose not to enforce a private debt. However, you need to be aware of the consequences first. The treatment differs depending on whether the loan is between two individuals, from an individual to a family trust, or from a company to a family member. Each scenario has different tax implications. There may be a love and affection exception for loans between individuals, but that same forgiveness may be treated as a gift by Centrelink, which could affect pension entitlements. Note that Centrelink’s gifting rules only activate where the forgiven amount exceeds $10,000 in a single financial year or $30,000 over five financial years — smaller forgiven debts may not trigger any pension impact. Once you forgive a debt you cannot unforgive it, so get financial and legal advice before you do so.

Colin: And who made the loan matters?

Andrew: Absolutely. If the loan was made by a family company rather than you personally, Division 7A of the Income Tax Assessment Act may deem that forgiveness to be a dividend paid to the shareholder, with real tax consequences for the company and the recipient. The cleanest approach for a personal debt forgiveness is a deed of forgiveness — a simple document recording that the debt will not be pursued further. Telling someone verbally or by email may not be sufficient if the ATO later asks questions.

Debt Collector Conduct: Your Rights Under the Australian Consumer Law

Applying the Australian Consumer Law (Schedule 2 to the Competition and Consumer Act 2010 (Cth)), ss 50–53.

📎 See also: Debt Collector Harassment Rights

Colin: Let us flip to the other side. What if someone is being harassed by a debt collector?

Andrew: Over the last few years the law has been significantly strengthened to protect people from unlawful debt collection conduct. Under the Australian Consumer Law, a debt collector cannot:

- Use physical force or coercion

- Call you at unreasonable hours

- Contact you an unreasonable number of times

- Discuss your debts with your employer, neighbours, or family without your consent

- Make any threats they are not legally entitled to make

- Mislead you about the amount you owe

- Threaten legal consequences that do not actually exist

Collectors who tell you they will “go to your workplace and embarrass you” or “tell your boss what you owe” are breaking the law. Breaching these provisions exposes the collector to civil penalties under the Australian Consumer Law, and the most serious conduct (such as threats or coercion) can also amount to criminal liability.

Caller 3 — Jason | Commercial Premises & Toilet Facilities

Jason (Caller): I called into a large food chain at Mermaid Waters and asked to use the toilet to wash my hands before eating, and was told they had no toilets. How can a business serving hundreds of customers a day legally operate without toilet facilities on site?

Andrew: It is an interesting question that touches on planning and building law. There are minimum requirements under the building code for businesses to have proper toilet and washroom facilities, particularly for staff. Whether those facilities must be accessible to the public depends on the individual development approval for that premises. In a shopping centre complex, the toilet may be part of the centre’s common facilities rather than the individual tenancy. If you want to follow it up, I would look at the building code — available online — and contact Gold Coast City Council, as the approval conditions for that specific business would be held by council.

Food Premises & Toilet Access: The Regulatory Framework

The rules governing toilet facilities at Queensland food businesses come from several overlapping sources:

- National Construction Code (Building Code of Australia): Sets the minimum number of toilets for commercial premises based on floor area. Food premises must comply. The number required scales with the size and occupancy of the venue.

- Australia New Zealand Food Standards Code (Standard 3.2.3): Requires food businesses to provide hand-washing facilities for food handlers (staff), but this obligation is to the staff, not to the public.

- Liquor Act 1992 (Qld) — Guideline 26: If the venue holds a liquor licence, it must provide patron-accessible toilets calculated in accordance with the Building Code. Toilets must be adequately lit and, where external, covered overhead.

- Development Approval Conditions: Each individual premises has a development approval issued by Gold Coast City Council. The specific conditions of that approval govern what facilities must be provided and accessible. In a shopping centre, patron toilet facilities are often part of the centre’s common-area approval rather than an individual tenancy’s DA.

What you can do: Contact Gold Coast City Council’s planning and development team and request the development approval conditions for that premises. If the DA requires patron toilet access and it was unavailable, that is a planning compliance matter reportable to Council. You can also contact Queensland Health directly — under Standard 3.2.3 of the Australia New Zealand Food Standards Code, hand-washing facilities must be located adjacent to toilet facilities and accessible to food handlers at all times. If the toilets were inaccessible, the compliant hand-washing station may also have been inaccessible, which is a food safety compliance matter.

📎 See also: Gold Coast City Council Development Enquiries

What To Do When a Debt Collector Crosses the Line

📎 See also: Debt Collector Harassment Rights

Colin: What should someone do if a debt collector is crossing the line?

Andrew: First, put your objection in writing directly to the debt collection company. Document every incident with dates, times, and what was said. If the conduct continues after your written objection, you have several escalation options: the ACCC, ASIC, and the Australian Financial Complaints Authority are all empowered to take complaints. Breaching these provisions exposes the collector to civil penalties under the Australian Consumer Law, and the most serious conduct (such as threats or coercion) can also amount to criminal liability. And importantly, just because you owe money does not mean your legal protections disappear.

Closing Summary

📎 See also: QCAT & Neighbourhood Disputes (Ep 7) | Debt Collection, EPoA & Wills (Ep 11)

Andrew: To summarise: if you are lending money that you cannot afford to lose, get it in writing before the money moves. If you are considering forgiving a debt, be aware there may be tax and Centrelink consequences and document the forgiveness properly. It is possible to document a loan after the fact with a deed, and partial payments are strong evidence of a loan in court. On when to involve a solicitor in debt collection matters: if the amount is over $25,000, you are in the Magistrates Court where costs are available to the winning party, so legal representation makes sense. Also get a solicitor if you have received a statutory demand, if there are mortgage or repossession actions, or if there are complicated factors making the loan difficult to evidence.

Disclaimer: This transcription provides general legal information only; it is not personal legal advice. Everyone’s situation is different, so please seek independent legal advice for your own circumstances.

Related Episodes

- Ep 11 — Debt Collection, EPoA vs AHD & The Cost of Wills — The episode this one directly continues, covering the PPSR, QCAT debt limits, and the difference between an Enduring Power of Attorney and an Advance Health Directive.

- Ep 10 — Off-the-Plan Property, Sunset Clauses & Executor Powers — Covers probate thresholds and Executor powers in detail, directly relevant to Bob’s call this episode.

- Ep 8 — Neighbour Disputes, Guardianship & Enforcing QCAT Decisions — Covers enforcing QCAT debt judgments and the practical realities of post-judgment collection.

- Ep 7 — QCAT & Neighbourhood Disputes — Overview of QCAT jurisdiction, costs rules, and how to file an application.